I am thinking about calling my credit card companies to see if I can get a decent balance transfer offer to pay off my HELOC. I get 0% offers all the time but I just shred them up. I don’t really want any more credit, I am trying to get rid of the debt that I have now.

I was thinking that I could transfer the balance of the HELOC (Currently at 10.25% or Prime + 2.5%) to a lower rate credit card, which will free up a portion of the $220 in interest that I pay per month.

The only downside I see to this is that I lose out on the mortgage interest deduction. I am hoping to have it paid off/refinanced before the end of the year but this transaction might save in excess of $1,000, which is probably a bigger benefit than the tax deduction. So far I have a 1.9% offer but it carries a fee that I can probably get waived.

I also opened a letter from my mortgage company today which said that I was pre-approved for a $20,000 increase in my home equity line. I initiated the increase just because I am currently maxed out on the line and the increase will improve my credit score if anything. There is a negative impact on your credit score the closer you are to the credit limit.

What do you think?

Friday, April 28, 2006

Thursday, April 27, 2006

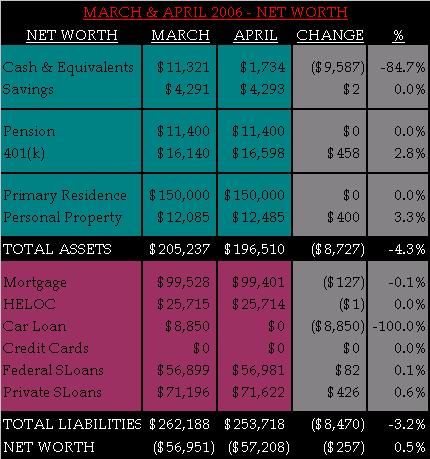

April Net Worth Recap…

Snapshot:

~ $400 over budget

Car loan got paid off

Only a $257 decline in net worth!

Eating out:

I got lazy in the last week. I stopped preparing lunches and cooking dinner and ate out a lot. $121 or 55% of eating out for the month came just in the last week alone.

Irregular expenses:

Irregular expenses for the month totaled $445 and primarily include: highlights $85 (every 4 months), clubhouse deposit $200, and the quarterly water bill $132. The irregular expenses basically account for the $400 over budget balance. Following my best friend’s bridal shower, I will be refunded $150 of the clubhouse deposit.

Personal expenses:

I also did not anticipate spending $103 in hair supplies this month. Vanity is expensive.

Summary:

This was a very good month and the best spending month in almost 6 years. I decided to stick with the Kelly Blue Book trade-in value for my auto to be conservative but I also added in my vested pension balance and restated my net worth. Now my net worth is ($57,208) as opposed to ($68,350). =) My car loan is now paid off so that means $500 in extra cash flow each month. I already committed $200 in extra cash to help pay down my HELOC in the coming months. Next month, I hope to curb the eating out expense even more and expect at least a $3000-3500 decline in my net worth since I have to pay for my summer class and books.

Go Chitowngirl…Improvement is in the works!!! =)

Wednesday, April 26, 2006

Used Car Value...

I got three estimates for the value of my car.

Kelley Blue Book: $12,485

Edmonds: $13,484

Nada: $15,875

I am going to go with the middle value in my net worth calculation.

Kelley Blue Book: $12,485

Edmonds: $13,484

Nada: $15,875

I am going to go with the middle value in my net worth calculation.

Edmonds or Kelley Blue Book…

I am trying to figure out the value of my car. I’ve been using Kelley’s trade-in-value but for some reason I see that most people use Edmonds.

Kelley Blue Book valued my car last month at $12,085.

Edmonds is valuing my car today at $15,895 for trade-in-value.

It is a 2002 Nissan with just 39,000 miles and it’s in good condition.

What do you think? Of course you know I want to use the value from Edmonds. =)

Kelley Blue Book valued my car last month at $12,085.

Edmonds is valuing my car today at $15,895 for trade-in-value.

It is a 2002 Nissan with just 39,000 miles and it’s in good condition.

What do you think? Of course you know I want to use the value from Edmonds. =)

Payday Looms…

Tomorrow is payday. Hallelujah!!!

I get to tally everything up for the month tonight and report the madness tomorrow morning. I also get to update my profile on networthiq.com and restate my net worth including my pension in my retirement assets. This should help out a lot.

All in all, I think I was overbudget by ~ $400. Bummer.

I get to tally everything up for the month tonight and report the madness tomorrow morning. I also get to update my profile on networthiq.com and restate my net worth including my pension in my retirement assets. This should help out a lot.

All in all, I think I was overbudget by ~ $400. Bummer.

Tuesday, April 25, 2006

Getting Financially Lazy…

In the last week, I have grown tremendously lazy. I haven’t cooked a thing. I’ve been eating out and I continue to blow the budget out of the water. I have to stop myself because I expect my net worth to decline each month for the next year and I don’t need to help it decline any further. I have to get it together. Just 2 more days and I can tally up the month and assess the damage. No matter what, it is sure to be the second best spending month in almost 6 years, which is an improvement in the right direction. =)

Monday, April 24, 2006

$40 Gas…

I just had to announce this. I spent $40 yesterday to fill p my gas tank...$2.99 per gallon for regular unleaded. Ouch!!!

I am so glad that I will be dropping down to 2 days of driving per week because gas prices are starting to take a big bit on the budget.

I am so glad that I will be dropping down to 2 days of driving per week because gas prices are starting to take a big bit on the budget.

Weekend Update and Month End Looming…

With the end of the month looming, I slipped big time this weekend with my spending. Now I am over budget for the month and it kind of stings. While this is a disappointment, it will still be the best spending month for me in almost 6 years. Definitely a positive! The goal is to curb my spending and learn to work within a budget so that when my income increases, I don’t increase my spending astronomically with it. That way, I can apply as much free cash flow to paying down student loan debt as possible.

Next month, I will have at least a $3,000 - $4,000 dip in my net worth because I have to pay for my summer class and books. Bummer but the end of school is near and I can finally see the light...One more year. (Chitowngirl is doing a dance over here!)

Next month, I will have at least a $3,000 - $4,000 dip in my net worth because I have to pay for my summer class and books. Bummer but the end of school is near and I can finally see the light...One more year. (Chitowngirl is doing a dance over here!)

Wednesday, April 19, 2006

Success Story…

The Motely Fool has a great article titled “Proof You Can Pay Off Your Debt”. The article details the story of a couple that eliminated $37,000 in consumer debt with a $60,000 salary. The best part is…they did it in just 17 months!!! Check out the story here.

Reading success stories of regular people working hard gives me hope that I will be debt free too one day. =)

Reading success stories of regular people working hard gives me hope that I will be debt free too one day. =)

Employee Pension Plan…

One of the reasons I opted to continue working full-time and to attend school part-time is because of BENEFITS!!! Sometimes I feel like I work for my benefits just as much as my salary. I also have a decent and generous employer. While I did get slighted along my career path, I was never totally jaded because the setbacks forced me to reconsider my career options and law school. So like most things, my first years out of undergrad were very bitter sweet.

I always knew that my employer had both a pension plan and a 401k plan. I never thought to include my pension plan in my net worth calculation because 1) I didn’t know how and 2) I was too lazy to figure it out. But I did some research today on the company’s website and have some good news to report.

401(k): My employer matches 100% of my 401k contributions up to 5% of my gross salary.

Account Balance: ~ $16,500

Employer Funded Pension: My pension is now fully vested and transferable, which means that I can take my vested account balance with me when I leave the company, no matter what my age is. Additionally, the pension plan has a long history and I have a very stable employer.

Account Balance: ~ $11,400.

So my total retirement benefits total $27,900. Oh yeah baby!!!

*When I do this month’s totals on networthiq.com, I will restate my net worth. =)

I always knew that my employer had both a pension plan and a 401k plan. I never thought to include my pension plan in my net worth calculation because 1) I didn’t know how and 2) I was too lazy to figure it out. But I did some research today on the company’s website and have some good news to report.

401(k): My employer matches 100% of my 401k contributions up to 5% of my gross salary.

Account Balance: ~ $16,500

Employer Funded Pension: My pension is now fully vested and transferable, which means that I can take my vested account balance with me when I leave the company, no matter what my age is. Additionally, the pension plan has a long history and I have a very stable employer.

Account Balance: ~ $11,400.

So my total retirement benefits total $27,900. Oh yeah baby!!!

*When I do this month’s totals on networthiq.com, I will restate my net worth. =)

Tuesday, April 18, 2006

Make Movies Affordable…

I had a great time going to the movies this weekend but spent a small fortune on snacks. The lesson? Bring snacks to the movie with you. Stop at the local grocery or convenient store on the way to the theatre and stock up on your favorite snacks. You can bet (and spend) your bottom dollar that the theatre has marked up the prices on the goodies at least double. Then you have all the pleasure of the treats and the entertainment but less financial guilt. The truth is that you can’t control the price of the movie tickets even at an early show, that’s a fixed cost. You can control the variable goodie cost and bring in your own snacks at a fraction of the cost. It's makes the experience that much more enjoyable. =)

Federal Student Loan Consolidation…

Today I will be attending a financial aid seminar at school dealing with federal loan consolidation. Once again, the rising interest rates are hitting the little man trying to make a better life for themselves and their families. The cost of higher education is just ridiculous.

I have to once again consolidate my student loans by June 1st to lock in a low rate of approximately 4.75%. After that, interest rates are rising to 6.8% for new Stafford loans and 8.5% for Plus loans. Ouch!!! I wonder how long student loan debt will be considered good debt if the interest rates are so high. Yahoo! had an article on it today. See here.

Unfortunately for me, I need to borrow for my last year of school and will not be able to consolidate those loans before the June 1st deadline. Therefore, I will have to borrower at the higher rate. Bummer. I also won’t be consolidating the last year of federal loans because they take a weighted average approach in fixing the interest rate. All in all, I will have about $55,000 fixed at approximately 4% and the rest of my student loan debt will have higher interest rates. Total Bummer but more incentive to pay the loans off quicker.

I have to once again consolidate my student loans by June 1st to lock in a low rate of approximately 4.75%. After that, interest rates are rising to 6.8% for new Stafford loans and 8.5% for Plus loans. Ouch!!! I wonder how long student loan debt will be considered good debt if the interest rates are so high. Yahoo! had an article on it today. See here.

Unfortunately for me, I need to borrow for my last year of school and will not be able to consolidate those loans before the June 1st deadline. Therefore, I will have to borrower at the higher rate. Bummer. I also won’t be consolidating the last year of federal loans because they take a weighted average approach in fixing the interest rate. All in all, I will have about $55,000 fixed at approximately 4% and the rest of my student loan debt will have higher interest rates. Total Bummer but more incentive to pay the loans off quicker.

Saturday, April 15, 2006

Preparation for Graduation...

Now that my car loan is paid off, I need to focus on what else needs to be accomplished before I finish law school and have to start paying back my student loans. (Chitowngirl cringes!) I don’t know if it is just my personality or what, but none of the other students seem to be worried about paying back their student loans. Even my closest friends aren’t worried and some have loans from undergrad as well. Maybe I am just more nervous since I never had student loans before law school.

So anyway...the plan is to pay off/refinance my home equity line by the end of September. This will free up another $200 in cash for a total of $900 in net free cash flow. Once the home equity line if paid off, the plan is to put any extra money into an emergency fund. With the inclusion of my student loans, my monthly expenses are going to skyrocket so I tried to calculate an adequate emergency fund. My short-term goal is 3 months or $14,000 which should be attainable with tuition reimbursement, any additional aid money, bonus and my tax return. I need to make sure that I can stash enough cash away to make sure that I can pay the monthly payments on my student loans should I not find a law job right away. I also have the option of placing some of the loans in forbearance should I need to do so. I hope not. So that’s the plan...I know I can do it.

So anyway...the plan is to pay off/refinance my home equity line by the end of September. This will free up another $200 in cash for a total of $900 in net free cash flow. Once the home equity line if paid off, the plan is to put any extra money into an emergency fund. With the inclusion of my student loans, my monthly expenses are going to skyrocket so I tried to calculate an adequate emergency fund. My short-term goal is 3 months or $14,000 which should be attainable with tuition reimbursement, any additional aid money, bonus and my tax return. I need to make sure that I can stash enough cash away to make sure that I can pay the monthly payments on my student loans should I not find a law job right away. I also have the option of placing some of the loans in forbearance should I need to do so. I hope not. So that’s the plan...I know I can do it.

*** I took a conservative approach to my emergency fund calculation:

- $200 in extra transportation (outside of insurance)

- $400 for health insurance (arbitrarily)

- Kept my standard of living the same

- Factored in full payment for student loans(I'm on a graudated payment schedule)

- Provided a $300 cushion

Thursday, April 13, 2006

Emergency Fund…

When I first approached calculating how much I needed in an emergency fund, I looked at my monthly committed expenses including groceries, subtracted out the “working” expenses that I wouldn’t incur (like commuting expenses) and then multiplied that figure by 6 months.

Is that right? I don’t think so anymore. I’ve read several things including the following:

Save 3-6 months of living expenses

Save 3-6 months of gross salary

Save 3-6 months of take home pay

Financial Train Wreck has a $12,000 emergency fund goal. Today he explained how he got to that figure after being prompted by a question from Mapgirl who has a $4,000 savings goal.

It is a really good post and informative as well. One major thing that I overlooked in my calculation was the cost of insurance and a cushion allowance for unexpected expenses and also expenses related to finding new employment. Needless to say...I have to go back to the drawing board.

So… How do you calculate the ideal amount of your emergency reserve?

Is that right? I don’t think so anymore. I’ve read several things including the following:

Save 3-6 months of living expenses

Save 3-6 months of gross salary

Save 3-6 months of take home pay

Financial Train Wreck has a $12,000 emergency fund goal. Today he explained how he got to that figure after being prompted by a question from Mapgirl who has a $4,000 savings goal.

It is a really good post and informative as well. One major thing that I overlooked in my calculation was the cost of insurance and a cushion allowance for unexpected expenses and also expenses related to finding new employment. Needless to say...I have to go back to the drawing board.

So… How do you calculate the ideal amount of your emergency reserve?

Wednesday, April 12, 2006

Preparation is Key…

I had a pretty bad cash flow day yesterday, spending $18 dollars on lunch, dinner and snacks. I am back on track. Now at first glance you may not think $18 is a lot of money but when you only have $300 to spend on whatever you want for the whole month, that $18 really takes a big bite out any future shopping I “may” decide to do. So, last night I forced myself to make my lunch for today to avoid any unnecessary spending. I also packed deli slices to snack on throughout the day. This should stave off my bad habit of snacking on chips. Yes…more bad habits. =)

Tuesday, April 11, 2006

Help…

I have an entry that I would like to post but I don’t know how to publish a range of cells from excel into my blog. I am so new to the blogging world but I am trying to Google to find out how to do it. If anyone has time to explain…please help if you can. Thanks in advance. I will be back soon. =)

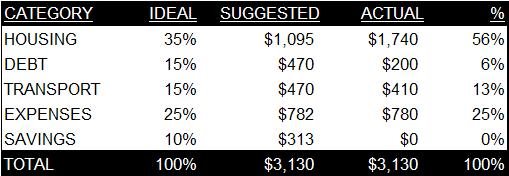

Debt Diet Monthly Spending Plan…

Jean Chatzky outlined the ideal monthly spending plan last week on Episode 5 of Oprah’s Debt Diet series. Below is a chart showing the ideal ratios, the suggested figure based on my take home pay and my actual expenses and ratios.

Note: I contribute 5% of my gross salary to my 401k and my employer matches it 100%. Take home pay is after 401k contributions, taxes, health care and insurance. These come out of my check each month before I take anything home.

Housing: First and second mortgage, assessments, security, electric, phone, cell phone, internet, and cable.

Debt: Currently I am paying additional on my home equity line to pay it off. Interest on my student loans is now capitalizing. The loans are not in prepayment while I am still in school.

Transportation: Car insurance, gas, parking.

Other: Hair salon visits (every other week), groceries, irregular expenses such as gifts and non-recurring expenses, and personal spending money.

Savings: Short-term and long-term.

Comments: This method is an eye opener for sure. I cannot tell you how horrible of a mess I was before I paid off my car loan just one week ago. Previously, my transportation ratio was 29% of my take home pay. Ouch!!!

As you can see, my housing ratio is extremely high. As a result, I have little to no additional income to put towards repayment of debt. After paying off my home equity line of credit this year, the housing ratio will only improve slightly and still be too high for my current income level. I resolve for now to stay in my condo. I only have one more year of law school after which I anticipate earning a higher salary.

By putting the figures into place, I have a better understanding of discretionary expenses versus committed expenses. This method allowed me see that I could decrease my discretionary expenses to put an extra $200 towards my home equity line.

My best friend's wedding is the only major planned expense for this year. I placed $500 in a separate checking account to contribute towards any additional wedding expenses. My dress is already paid for and I already booked the facility for her Bridal Shower. Plus, there are 8 other bridesmaids to contribute to expenses. =)

BTW...this while HTML thing is so hard but hopefully I will get it figured out soon. =)

Note: I contribute 5% of my gross salary to my 401k and my employer matches it 100%. Take home pay is after 401k contributions, taxes, health care and insurance. These come out of my check each month before I take anything home.

Housing: First and second mortgage, assessments, security, electric, phone, cell phone, internet, and cable.

Debt: Currently I am paying additional on my home equity line to pay it off. Interest on my student loans is now capitalizing. The loans are not in prepayment while I am still in school.

Transportation: Car insurance, gas, parking.

Other: Hair salon visits (every other week), groceries, irregular expenses such as gifts and non-recurring expenses, and personal spending money.

Savings: Short-term and long-term.

Comments: This method is an eye opener for sure. I cannot tell you how horrible of a mess I was before I paid off my car loan just one week ago. Previously, my transportation ratio was 29% of my take home pay. Ouch!!!

As you can see, my housing ratio is extremely high. As a result, I have little to no additional income to put towards repayment of debt. After paying off my home equity line of credit this year, the housing ratio will only improve slightly and still be too high for my current income level. I resolve for now to stay in my condo. I only have one more year of law school after which I anticipate earning a higher salary.

By putting the figures into place, I have a better understanding of discretionary expenses versus committed expenses. This method allowed me see that I could decrease my discretionary expenses to put an extra $200 towards my home equity line.

My best friend's wedding is the only major planned expense for this year. I placed $500 in a separate checking account to contribute towards any additional wedding expenses. My dress is already paid for and I already booked the facility for her Bridal Shower. Plus, there are 8 other bridesmaids to contribute to expenses. =)

BTW...this while HTML thing is so hard but hopefully I will get it figured out soon. =)

Sunday, April 09, 2006

Condo Market Value...

Occasionally I do a search for condos that go on the market in my suburb and the neighboring suburb to compare valuations. The condos in my complex and my sister’s complex are built exactly the same. Even though we literally live less than a mile away down the street, she technically lives in another city.

The value of the condos in my complex have always outpaced hers so it was very interesting when I saw a 3 bedroom, 2 bathroom unit on the market for $175,000 in her complex. The description does say the unit was newly rehabbed with whirlpool tub, new kitchen with granite counter tops, hardwood flooring in living room, dining room and kitchen, carpeted bedrooms, recessed lights, and all new drywall. This sounds like the place was a mess and they did a complete gut rehab.

I have a 3 bedroom, 2 bath unit. I recently put in wood flooring in the living room, dining room, and kitchen and also replaced the carpeting in the bedrooms. With the exception of my washer/dryer unit, all of my appliances are relatively new and in wonderful shape. Actually, my unit in and of itself is very nice and in good shape.

I currently value my unit at $150,000. Even though I didn’t do a gut rehab because it didn’t need it, I wonder if I am undervaluing my condo unit. Zillow.com estimates the value at $171,000. It will be very interesting to see what the unit sells for and I will be keeping my eye out for notices of recent sales. This could prove wonderful for my net worth...Any improvement would be great. =)

The value of the condos in my complex have always outpaced hers so it was very interesting when I saw a 3 bedroom, 2 bathroom unit on the market for $175,000 in her complex. The description does say the unit was newly rehabbed with whirlpool tub, new kitchen with granite counter tops, hardwood flooring in living room, dining room and kitchen, carpeted bedrooms, recessed lights, and all new drywall. This sounds like the place was a mess and they did a complete gut rehab.

I have a 3 bedroom, 2 bath unit. I recently put in wood flooring in the living room, dining room, and kitchen and also replaced the carpeting in the bedrooms. With the exception of my washer/dryer unit, all of my appliances are relatively new and in wonderful shape. Actually, my unit in and of itself is very nice and in good shape.

I currently value my unit at $150,000. Even though I didn’t do a gut rehab because it didn’t need it, I wonder if I am undervaluing my condo unit. Zillow.com estimates the value at $171,000. It will be very interesting to see what the unit sells for and I will be keeping my eye out for notices of recent sales. This could prove wonderful for my net worth...Any improvement would be great. =)

Friday, April 07, 2006

Oprah’s Debt Diet...

Watching the Debt Diet has been a BIG turning point for me. Until then, I knew I was in trouble financially but I didn’t have the motivation or guidance to do anything about it. When I had money in my checking account, I didn’t feel broke. (Even if the money was financial aid debt that I would eventually have to pay back.) Meanwhile, my net worth declined and I knew it. What I am trying to say is that despite the fact that I’ve been keeping count of my declining net worth for years, I did nothing to change my attitude or my spending behavior. I had this mindset that one day it would all get fixed. One day I would make more money and all would be well in Chitowngirl’s world.

I see a lot of myself in Brenda Bradley. She wanted the big house, the fancy cars, she liked to shop, eat out, etc. Well...who the heck doesn’t? I certainly do and I got a lot of things to my detriment. The difference between me and Brenda Bradley is that I decided to do something sooner rather than later. I decided to change my behavior before I could have the chance to put the financial and emotional drain on a marriage or hamper my children’s future. That is the only difference. Financial awakening happens for people at different times. I feel so grateful that the time for me is NOW.

I went on the message boards and saw the mean comments about the Bradley’s and Brenda in particular. Quite frankly, I was appalled at what I read. Why judge? Some people spend for a variety of reasons and everyone has had a different upbringing. Some were exposed to financial lessons, others learned from what they saw. As Oprah said... “When you know better...You can do better!” She said this one day and it struck a cord. I know my spending behavior is hurting me now and the more I continue down this destructive path, the more it is going to hurt my future.

I am thankful for the show and I am thankful that these families had the courage to put it all out there and make a positive change in their lives. So instead of judging, I salute them and I hope they have much success because...

When you know better...You can do better!!!

I see a lot of myself in Brenda Bradley. She wanted the big house, the fancy cars, she liked to shop, eat out, etc. Well...who the heck doesn’t? I certainly do and I got a lot of things to my detriment. The difference between me and Brenda Bradley is that I decided to do something sooner rather than later. I decided to change my behavior before I could have the chance to put the financial and emotional drain on a marriage or hamper my children’s future. That is the only difference. Financial awakening happens for people at different times. I feel so grateful that the time for me is NOW.

I went on the message boards and saw the mean comments about the Bradley’s and Brenda in particular. Quite frankly, I was appalled at what I read. Why judge? Some people spend for a variety of reasons and everyone has had a different upbringing. Some were exposed to financial lessons, others learned from what they saw. As Oprah said... “When you know better...You can do better!” She said this one day and it struck a cord. I know my spending behavior is hurting me now and the more I continue down this destructive path, the more it is going to hurt my future.

I am thankful for the show and I am thankful that these families had the courage to put it all out there and make a positive change in their lives. So instead of judging, I salute them and I hope they have much success because...

When you know better...You can do better!!!

Thursday, April 06, 2006

Free Food…

You just have to love free food at work. I was starving around one o’clock this afternoon and I began thinking about buying soup from the café to go with my sandwich. Well, low and behold, someone filled me in on the fact that pizza was ordered for the floor since there were so many birthdays. Needless to say…my tummy is very happy. Yippee!!!

Fighting the Shopping Urge…

The desire to shop is starting to eat at me. Generally speaking, I am not a regular shopper because I rather do it all at once. I must have some residual hard feelings from working retail because I am not a huge mall or crowd fan. I usually shop when Summer is on the way and again in the Fall. It is during these times that I spent quite a bit of money but I don’t buy anything in between unless I have to.

The thing is that I don’t “need” anything. My current workplace has a business casual dress policy but with graduation approaching, I am thinking that I need to purchase more suiting rather than casual clothes. A nice suit can cost but in actuality it saves in the long run financially. You can wear a suit more than once and just change out the shell or blouse. Right now, it costs $8 to get a twin set cleaned because they count each item separately. Dryel is my friend and I swear they totally cheat women at the dry cleaners but I will save that rant for another day. (Chitowngirl takes in deep breaths… LOL) Plus it saves time because it makes deciding what to wear a whole lot easier.

So…future investments in work clothing will have a bigger focus on acquiring suits. Now I don’t have the huge urge to shop because I don’t have the money to spend $100’s on a suit.

Done deal. =)

The thing is that I don’t “need” anything. My current workplace has a business casual dress policy but with graduation approaching, I am thinking that I need to purchase more suiting rather than casual clothes. A nice suit can cost but in actuality it saves in the long run financially. You can wear a suit more than once and just change out the shell or blouse. Right now, it costs $8 to get a twin set cleaned because they count each item separately. Dryel is my friend and I swear they totally cheat women at the dry cleaners but I will save that rant for another day. (Chitowngirl takes in deep breaths… LOL) Plus it saves time because it makes deciding what to wear a whole lot easier.

So…future investments in work clothing will have a bigger focus on acquiring suits. Now I don’t have the huge urge to shop because I don’t have the money to spend $100’s on a suit.

Done deal. =)

Wednesday, April 05, 2006

Excited…

I just have to say that I am really excited because for the first time in three years since I purchased my condo and started law school, I feel encouraged. I have a positive outlook on the future and good financial plan.

Financially I may not be where I thought I would be at this time in my life (quickly approaching thirty) but I am healthy, I have a wonderful family, I have a home, a job, and I am almost through with law school. I’ve accomplished a lot in the last three years and for that, I need to hold my head up high.

For the past 3 years, I have worked my butt off going to school 4 nights a week while working full time. I even made the Dean’s List last semester. =) I could have taken the easy route and quit working and lived completely off financial aid but I can promise you…the net worth chart on this page would look a whole lot worse. While I stumbled pretty badly along the way…I am still standing and I know things will get better if I continue to work hard and make the best decisions possible.

Staying positive is the best antidote to having tons of debt. =)

Financially I may not be where I thought I would be at this time in my life (quickly approaching thirty) but I am healthy, I have a wonderful family, I have a home, a job, and I am almost through with law school. I’ve accomplished a lot in the last three years and for that, I need to hold my head up high.

For the past 3 years, I have worked my butt off going to school 4 nights a week while working full time. I even made the Dean’s List last semester. =) I could have taken the easy route and quit working and lived completely off financial aid but I can promise you…the net worth chart on this page would look a whole lot worse. While I stumbled pretty badly along the way…I am still standing and I know things will get better if I continue to work hard and make the best decisions possible.

Staying positive is the best antidote to having tons of debt. =)

Next Goal…

Next goal: Use my tuition reimbursement and next year’s bonus and tax return to pay off my home equity line of credit. This will free up an additional $200 in monthly cash flow.

Shortly after that, I should graduate from law school with just my first mortgage and student loan debt. Then my hope is to pay off the student loans in chunks, starting with the private loans. My federal loans have a very low interest rate so I won’t worry much about those in the near future. The interest rates on the private loans are much higher so I will pay those off with any extra money coming into the house such as bonuses and any tax returns that I receive. I plan to use the snowball method to pay them off from the smallest loan amount (~ $5,000) to the highest loan amount (~ $21,000). I do not plan to reduce my retirement contribution just because the student loans come due but this method will free up additional cash flow along the way.

Shortly after that, I should graduate from law school with just my first mortgage and student loan debt. Then my hope is to pay off the student loans in chunks, starting with the private loans. My federal loans have a very low interest rate so I won’t worry much about those in the near future. The interest rates on the private loans are much higher so I will pay those off with any extra money coming into the house such as bonuses and any tax returns that I receive. I plan to use the snowball method to pay them off from the smallest loan amount (~ $5,000) to the highest loan amount (~ $21,000). I do not plan to reduce my retirement contribution just because the student loans come due but this method will free up additional cash flow along the way.

Tuesday, April 04, 2006

Slippery Slope…

Eating out for me is a slippery slope. For some it starts with a simple coffee at Starbucks but for me it might start with a snack from the café between classes. Then I start spending a dollar here and a dollar there. I say to myself…it’s just a few bucks. Before I know it, I spent $20 bucks.

So today I spent $4 on snacks…I need to reel it in before it gets out of hand. I would rather use my discretionary money to make a meaningful purchase like a new pair of workout shoes, a small stock investment, or save for a vacation. That is meaningful...not snacks that spend a second on the lips and a lifetime on the hips. LOL.

So today I spent $4 on snacks…I need to reel it in before it gets out of hand. I would rather use my discretionary money to make a meaningful purchase like a new pair of workout shoes, a small stock investment, or save for a vacation. That is meaningful...not snacks that spend a second on the lips and a lifetime on the hips. LOL.

Car Loan Paid Off…

I did it!!! I finally did it!!!

The pay off depleted most of my savings but it just made sense. I wasn’t earning nearly as much interest in my checking account as I was paying on the car loan, which was at approximately 5.6%. Next step will be to pay off my $25,000 home equity line and then all I will have in the way of debts is my first mortgage and my student loans.

Currently my home equity line of credit is at Prime + 2.5%, or 10.25%. The rate is so high because at the initial purchase, the loan to value was 100%. I’ve been rather lazy at refinancing the loan, which could give me an interest rate at Prime or even Subprime. I need to get on it! (Chitowngirl shakes her head) I don’t feel that bad about the home equity line because it is not debt that I acquired by personal spending. It was the result of an 80/20 mortgage, which is what I needed to buy my place at the time. My condo has appreciated approximately $20,000 since I bought it three years ago and I recently did some remodeling (I know…don’t blast me!!!) which cost me thousands to put in new wood floors, carpeting in three bedrooms, and to re-stain my kitchen cabinets as opposed to replacing them.

When I look back on it, I know I should have held off on the complete overhaul and just put down new carper. It had to be replaced. White carpet just does not work well in the City of Unpredictable Weather. Plus…I just told you… I am lazy about some things so I hardly ever took my shoes off right away. Now with the floors…I have no worries.

One more reason why I did the project was that I knew I would be in my place for a while to come. Why? I simply cannot afford anything else with the mounting student loans, no guaranteed higher paying position after school is over, and rising real estate prices and interest rates. So, I finally made it feel like home and I settled in for the long run…at least 5 years.

Chitowngirl does a little dance…Car loan…PAID!!!

The pay off depleted most of my savings but it just made sense. I wasn’t earning nearly as much interest in my checking account as I was paying on the car loan, which was at approximately 5.6%. Next step will be to pay off my $25,000 home equity line and then all I will have in the way of debts is my first mortgage and my student loans.

Currently my home equity line of credit is at Prime + 2.5%, or 10.25%. The rate is so high because at the initial purchase, the loan to value was 100%. I’ve been rather lazy at refinancing the loan, which could give me an interest rate at Prime or even Subprime. I need to get on it! (Chitowngirl shakes her head) I don’t feel that bad about the home equity line because it is not debt that I acquired by personal spending. It was the result of an 80/20 mortgage, which is what I needed to buy my place at the time. My condo has appreciated approximately $20,000 since I bought it three years ago and I recently did some remodeling (I know…don’t blast me!!!) which cost me thousands to put in new wood floors, carpeting in three bedrooms, and to re-stain my kitchen cabinets as opposed to replacing them.

When I look back on it, I know I should have held off on the complete overhaul and just put down new carper. It had to be replaced. White carpet just does not work well in the City of Unpredictable Weather. Plus…I just told you… I am lazy about some things so I hardly ever took my shoes off right away. Now with the floors…I have no worries.

One more reason why I did the project was that I knew I would be in my place for a while to come. Why? I simply cannot afford anything else with the mounting student loans, no guaranteed higher paying position after school is over, and rising real estate prices and interest rates. So, I finally made it feel like home and I settled in for the long run…at least 5 years.

Chitowngirl does a little dance…Car loan…PAID!!!

Monday, April 03, 2006

Confession…

I still haven’t paid off my car loan. I know…I know…the $12,000 is just sitting in my account and I need to go on and stop procrastinating and just pay the darn $9,000 off so I can free up $500 a month in cash flow. I still have this mental block saying…I am going to be broke. I have a fear…a big fear…of being broke! =(

My financial tailspin began my freshman year of college. I ran out of money…on the weekend nonetheless. So Mom and Dad couldn’t just deposit available funds into my account or drive 50 miles up the north shore to bring me some cash. I remember being embarrassed. A few of my friends had asked me to do out to dinner with them and I said sure. I thought I had money…Chitowngirl was never without money. I made up some lame excuse for why I couldn’t go with them and then called my Mom crying…which made her feel bad…like she was a bad Mom for not providing for me.

6 years later, I STILL feel bad and ashamed of this because my parents are wonderful and have ALWAYS provided for me. It was completely my fault that I ran out of money in the first place. I blew through it like it was nothing. I didn’t realize or mentally process that I was spending my parents’ hard earned money. I didn’t know the value of a dollar.

Soon after, I tried to get a credit card but was denied for lack of financial history. I didn’t try for the cheesy t-shirt cards. A few months later…not only did I get approved for a credit card, but I got pre-approved for a credit card with a limit of $11,000. What on earth would a 19/20 year old do with that kind of credit limit? All in all, I graduated with $4,000 in credit card debt.

6 years later… I am still learning. Except now, I am spending my hard earned money and realizing just how much I have to work to buy this or that. When I think about having to work two weeks just to buy something, it makes me not want it that bad. Right now I feel like I placed myself into a form of servitude…working to pay off my debt.

I wasn’t a rich kid. I come from a middle class family who worked hard to give their children the best opportunities in life. I just didn’t understand the value of a dollar. I DO NOW! =)

My financial tailspin began my freshman year of college. I ran out of money…on the weekend nonetheless. So Mom and Dad couldn’t just deposit available funds into my account or drive 50 miles up the north shore to bring me some cash. I remember being embarrassed. A few of my friends had asked me to do out to dinner with them and I said sure. I thought I had money…Chitowngirl was never without money. I made up some lame excuse for why I couldn’t go with them and then called my Mom crying…which made her feel bad…like she was a bad Mom for not providing for me.

6 years later, I STILL feel bad and ashamed of this because my parents are wonderful and have ALWAYS provided for me. It was completely my fault that I ran out of money in the first place. I blew through it like it was nothing. I didn’t realize or mentally process that I was spending my parents’ hard earned money. I didn’t know the value of a dollar.

Soon after, I tried to get a credit card but was denied for lack of financial history. I didn’t try for the cheesy t-shirt cards. A few months later…not only did I get approved for a credit card, but I got pre-approved for a credit card with a limit of $11,000. What on earth would a 19/20 year old do with that kind of credit limit? All in all, I graduated with $4,000 in credit card debt.

6 years later… I am still learning. Except now, I am spending my hard earned money and realizing just how much I have to work to buy this or that. When I think about having to work two weeks just to buy something, it makes me not want it that bad. Right now I feel like I placed myself into a form of servitude…working to pay off my debt.

I wasn’t a rich kid. I come from a middle class family who worked hard to give their children the best opportunities in life. I just didn’t understand the value of a dollar. I DO NOW! =)

It’s Raining Like Cats and Dogs…

This morning it was raining so badly and to top things off…I was so unorganized. I had my HUGE backpack, my shoulder bag with my purse in it, my lunch sack, my coffee cup, and yes folks…my UMBRELLA. I looked like a hot mess walking through the Windy City with the rain blowing every which way, threatening at every moment to blow inside out. LOL. Needless to say…I arrived to work very wet…soaked to the toes. Oh yeah…it is going to be a wonderful week. =)

One good thing…This morning while running late, I remembered that now that I will be riding the train, I won’t get home tonight until roughly 10:30. Ouch!!! So, I needed to pack a snack for the train ride home, which will constitute my dinner. The bad part…the sandwich I made was a quick PB&J sandwich but the good part…I saved about $5-7 by making it. =)

One good thing…This morning while running late, I remembered that now that I will be riding the train, I won’t get home tonight until roughly 10:30. Ouch!!! So, I needed to pack a snack for the train ride home, which will constitute my dinner. The bad part…the sandwich I made was a quick PB&J sandwich but the good part…I saved about $5-7 by making it. =)

Sunday, April 02, 2006

Another Day…Another Good Day…

I spent $0 dollars today people….Zero…Zippo!!!

I have to thank my Mom and Dad for the dinner invite and my Mom for making a wonderful meal. I even have leftovers for lunch tomorrow. =)

I am kind of dreading work tomorrow. A main expressway in Chicago is getting a major overhaul over the next 2 years and they didn’t even ask my permission for the inconvenience. LOL. I drive it 3 days a week and now I’ve been banished to the train. It’s cool…we have an awesome train system that will get me to and from work and school just fine. You have to be grateful for something like that.

Chitowngirl is doing a happy dance over here!!! I had a wonderful weekend. =)

I have to thank my Mom and Dad for the dinner invite and my Mom for making a wonderful meal. I even have leftovers for lunch tomorrow. =)

I am kind of dreading work tomorrow. A main expressway in Chicago is getting a major overhaul over the next 2 years and they didn’t even ask my permission for the inconvenience. LOL. I drive it 3 days a week and now I’ve been banished to the train. It’s cool…we have an awesome train system that will get me to and from work and school just fine. You have to be grateful for something like that.

Chitowngirl is doing a happy dance over here!!! I had a wonderful weekend. =)

Saturday, April 01, 2006

Grocery Shopping…

I just got back from grocery shopping and I was nice and just a little bit naughty. =)

The Grand Total….A whopping $122!!!

I know that seems like a lot but I have to tell you that I am so pleased with my shopping experience. You’ll see why…

I already had frozen chicken breast in the deep freezer but that was it. So I decided to go to Sam’s Club and get all the rest of my meats for the month to add some variety. While there I found that they had frozen salmon individually wrapped. Since salmon was on my grocery list already, I decided this would probably work out more economically and last for several more months. Good find indeed. Also while I was there, I decided to get a few other cuts of meat (steak and pork chops) and immediately came home and individually wrapped them in freezer bags. This will make defrosting and portion control a lot easier. Thanks Rachel Ray for the tip!!!

So all in all, I have meat covered not just for one month but at least two or more. This is definitely a thumbs up for Chitowngirl!!!

I rounded off the remainder of my shopping with soda, veggies for the week, what I need to make cold cut sandwiches, and a few household toiletries. I am so covered it is not even funny. No fast food for me. LOL.

My monthly grocery/household budget is $150. So I still have some money left to purchase fresh veggies, frozen if they go on sale, and/or any other needs. I should make it just fine.

*** I have to say this because I am so tickled. It is already the third day into this month’s budget and I only spent $5 in discretionary money out of $300. Usually, I would have already blown through at least $40 bucks. This blog and is already starting to help. Oh yeah baby!!!

The Grand Total….A whopping $122!!!

I know that seems like a lot but I have to tell you that I am so pleased with my shopping experience. You’ll see why…

I already had frozen chicken breast in the deep freezer but that was it. So I decided to go to Sam’s Club and get all the rest of my meats for the month to add some variety. While there I found that they had frozen salmon individually wrapped. Since salmon was on my grocery list already, I decided this would probably work out more economically and last for several more months. Good find indeed. Also while I was there, I decided to get a few other cuts of meat (steak and pork chops) and immediately came home and individually wrapped them in freezer bags. This will make defrosting and portion control a lot easier. Thanks Rachel Ray for the tip!!!

So all in all, I have meat covered not just for one month but at least two or more. This is definitely a thumbs up for Chitowngirl!!!

I rounded off the remainder of my shopping with soda, veggies for the week, what I need to make cold cut sandwiches, and a few household toiletries. I am so covered it is not even funny. No fast food for me. LOL.

My monthly grocery/household budget is $150. So I still have some money left to purchase fresh veggies, frozen if they go on sale, and/or any other needs. I should make it just fine.

*** I have to say this because I am so tickled. It is already the third day into this month’s budget and I only spent $5 in discretionary money out of $300. Usually, I would have already blown through at least $40 bucks. This blog and is already starting to help. Oh yeah baby!!!

Just Rambling...

It looks like a pretty gloomy day here in Chicago after an absolutely beautiful day yesterday. Spring is on its way and I cannot wait!

I woke up this morning exhausted. I cannot wait for this law school thing to end. Working full-time and going to school part-time is no joke. I get on average about 5 hours of sleep every night. Wowsa!!! So by the weekend, I am trying to log in as much sleep as I can. LOL.

So right now, I am making a grocery list and checking it twice. When I get to the store, I am going to find out if I’m naughty or nice. LOL. I just really hope that I can stick to my budget and what’s on my list. I am trying to think of realistic things to prepare that would be easy to transport to work.

I also need to wash my car this weekend. To cut costs, I am going to drag my vacuum out to the garage and clean it out with the attachments and then spend just $3-5 with my coupon to wash the outside. In Chicago you have to make sure you don’t keep too much salt on your car because it will eat away at the paint. (At least I think that's true. LOL)

So this weekend, I am trying to spend as little discretionary money as possible. I tend to go a little crazy on the weekend but if I really want to keep my spending to my earnings and not use any debt, then my new budget only allows $300 to spend on whatever I want. Now I thought about it...What do I really want? Some new workout shoes, highlights for my hair, and I want to be DEBT FREE. I made it so that any eating out comes from my discretionary money so I have an incentive to stick with the food I buy with my grocery budget and eat at home. With the leftover money, I can either 1) open a Sharebuilder account, 2) open a high yield savings account or 3) allocate it to my home equity line.

I don't have any credit card debt. Outside of my student loans, the only debt I have is my car loan that I’m paying off this month with my savings and my HELOC (never used for personal expense, just the home purchase). So any extra money should go to my HELOC or to savings. I don't want it sitting in my checking account. Dangerous I tell you...Dangerous. =)

Have a wonderful weekend everyone!!!

I woke up this morning exhausted. I cannot wait for this law school thing to end. Working full-time and going to school part-time is no joke. I get on average about 5 hours of sleep every night. Wowsa!!! So by the weekend, I am trying to log in as much sleep as I can. LOL.

So right now, I am making a grocery list and checking it twice. When I get to the store, I am going to find out if I’m naughty or nice. LOL. I just really hope that I can stick to my budget and what’s on my list. I am trying to think of realistic things to prepare that would be easy to transport to work.

I also need to wash my car this weekend. To cut costs, I am going to drag my vacuum out to the garage and clean it out with the attachments and then spend just $3-5 with my coupon to wash the outside. In Chicago you have to make sure you don’t keep too much salt on your car because it will eat away at the paint. (At least I think that's true. LOL)

So this weekend, I am trying to spend as little discretionary money as possible. I tend to go a little crazy on the weekend but if I really want to keep my spending to my earnings and not use any debt, then my new budget only allows $300 to spend on whatever I want. Now I thought about it...What do I really want? Some new workout shoes, highlights for my hair, and I want to be DEBT FREE. I made it so that any eating out comes from my discretionary money so I have an incentive to stick with the food I buy with my grocery budget and eat at home. With the leftover money, I can either 1) open a Sharebuilder account, 2) open a high yield savings account or 3) allocate it to my home equity line.

I don't have any credit card debt. Outside of my student loans, the only debt I have is my car loan that I’m paying off this month with my savings and my HELOC (never used for personal expense, just the home purchase). So any extra money should go to my HELOC or to savings. I don't want it sitting in my checking account. Dangerous I tell you...Dangerous. =)

Have a wonderful weekend everyone!!!

My Vice...

My financial vice is eating out.

With my work and evening class schedule, my days often extend 15-16 hours and I have very little time for cooking. Plus, I need to face it…I don’t know how to cook that well but I am in the process of learning and finding it surprisingly fun.

So in an effort to curb spending on food, I upped my grocery budget so I can get a better handle on this expense. I spent almost $500 alone on lunches and dinners last month and that has to stop. That is at least $200 that can go towards paying off my HELOC or finally starting an investment account.

Today I made both lunch and dinner. (Chitowngirl pats herself on the back) I found that I enjoyed the food much better and I felt good about eating healthier and knowing exactly what was in my meal. Plus, I have enough leftover for breakfast tomorrow. Oh yeah!!!

Wish me well. At least I have good homeowner’s insurance in case I have any kitchen disasters. LOL.

With my work and evening class schedule, my days often extend 15-16 hours and I have very little time for cooking. Plus, I need to face it…I don’t know how to cook that well but I am in the process of learning and finding it surprisingly fun.

So in an effort to curb spending on food, I upped my grocery budget so I can get a better handle on this expense. I spent almost $500 alone on lunches and dinners last month and that has to stop. That is at least $200 that can go towards paying off my HELOC or finally starting an investment account.

Today I made both lunch and dinner. (Chitowngirl pats herself on the back) I found that I enjoyed the food much better and I felt good about eating healthier and knowing exactly what was in my meal. Plus, I have enough leftover for breakfast tomorrow. Oh yeah!!!

Wish me well. At least I have good homeowner’s insurance in case I have any kitchen disasters. LOL.

Subscribe to:

Posts (Atom)