Note: I contribute 5% of my gross salary to my 401k and my employer matches it 100%. Take home pay is after 401k contributions, taxes, health care and insurance. These come out of my check each month before I take anything home.

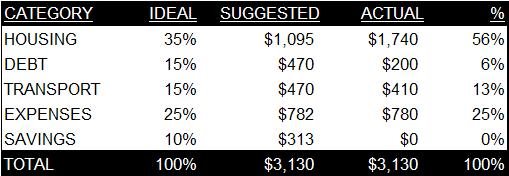

Housing: First and second mortgage, assessments, security, electric, phone, cell phone, internet, and cable.

Debt: Currently I am paying additional on my home equity line to pay it off. Interest on my student loans is now capitalizing. The loans are not in prepayment while I am still in school.

Transportation: Car insurance, gas, parking.

Other: Hair salon visits (every other week), groceries, irregular expenses such as gifts and non-recurring expenses, and personal spending money.

Savings: Short-term and long-term.

Comments: This method is an eye opener for sure. I cannot tell you how horrible of a mess I was before I paid off my car loan just one week ago. Previously, my transportation ratio was 29% of my take home pay. Ouch!!!

As you can see, my housing ratio is extremely high. As a result, I have little to no additional income to put towards repayment of debt. After paying off my home equity line of credit this year, the housing ratio will only improve slightly and still be too high for my current income level. I resolve for now to stay in my condo. I only have one more year of law school after which I anticipate earning a higher salary.

By putting the figures into place, I have a better understanding of discretionary expenses versus committed expenses. This method allowed me see that I could decrease my discretionary expenses to put an extra $200 towards my home equity line.

My best friend's wedding is the only major planned expense for this year. I placed $500 in a separate checking account to contribute towards any additional wedding expenses. My dress is already paid for and I already booked the facility for her Bridal Shower. Plus, there are 8 other bridesmaids to contribute to expenses. =)

BTW...this while HTML thing is so hard but hopefully I will get it figured out soon. =)

1 comment:

You did an excellent job with that table! now you need to show me. LOL

My rent is within the recommended percentage, but after I move into the house, it'll exceed 50%. With the housing market the way it is, I don't know how one can stay below 35% with one income. I think I'm doing ok with the other categories but there's always room for improvement. BTW, this is a great post. I've always seen the recommended expense ratios, but have never analyzed my own. You've inspired me, so now I'm about to steal your idea. LOL

Congrats to your best friend and her upcoming nuptials!!

Post a Comment