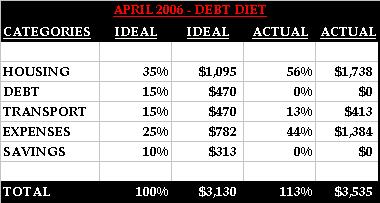

Debt Diet: My actual spending definitely does not conform to the Debt Diet plan.

Housing: I have little control over this figure for now. Currently, I am focusing on paying off my HELOC which totals approximately $25,700 and hopefully with a salary increase next year I will fall more in line with the recommended 35% ratio.

Debt: Currently I don’t pay anything on my student loans and the interest is capitalizing to the tune of ~$500/month. Debt repayment will begin 6-9 months following my May 2007 graduation.

Transportation: Thank goodness one category meets the recommended ratio. I anticipate this figure to improve after my May graduation next year since I will no longer need to drive downtown and park. I can revert back to taking the train.

Expenses: I need to focus on reducing personal expenses. I have a lot of control over my spending so I definitely need to do better in this area. I am getting better but there is always room for more improvement.

Savings: No after-tax savings at this time. Right now and I’m focused on paying off debt. I do however contribute 5% of my gross salary to my 401k, which my employer matches. So every month, ~$450 goes into my 401k.

2 comments:

This is why I don't like Jean Chatzky's Debt Diet spending plan. You're "supposed to" have $470 in debt payments?

Theoretically I believe the goal under the plan is to cap debt repayment to 15% of your monthly take home. Therefore the amount of debt payments should never exceed 15%. If it does then you have too much debt and have to cut from the other categories.

I believe the ultimate goal is to have a balanced financial picture so that you can achieve all the goals of necessities, debt repayment, savings, and living.

I am very unbalanced at this point. =)

Post a Comment