September was a better month. I moved to a cash only system and steered away from the use of credit cards. It was a lot less stressful and I could feel the pain of my cash balances declining throughout the month. Irregular expenses and purchases hit me hard in September and they are hitting me hard in October as well. I can say that all October irregular expenses thus far have been necessary expenses and not discretionary like my new PDA/Cell Phone that I purchased in September. I purchased it so that I can keep up with all my appointments/interviews, work meetings, school projects, exams, and assignments due.

Irregular Expenses: ~ $1,300 (OUCH!!!). I don’t have to tell you that this completely threw my budget out the window. Luckily, I got $900 extra in September in tuition reimbursement that helped out a lot.

Interview Expenses: $330

Law School MPRE Exam: $60

Car Repairs: $260

New PDA/Cell Phone: $380 - $100 Mail in Rebate so $280

New Computer Battery: $80

Garage Door Repair: $100

Birthday Gifts: $100

Discretionary Spending: ~ $1200. Once again, I spent way too much but I know it would have been worse using my CC. Not so much on clothing or anything like that, just eating out and entertainment spending. This spending would be in line with a salary in the $135k range, not my $54k salary.

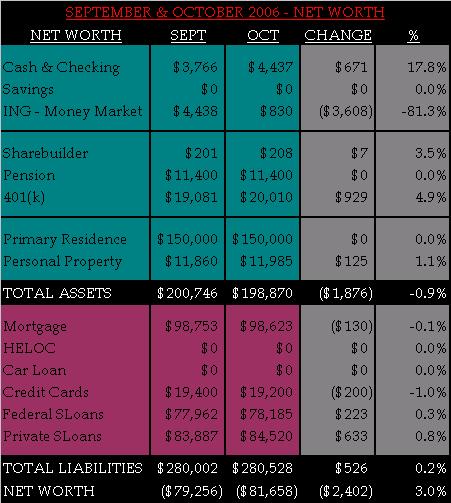

Savings: I transferred $4,000 of my Savings into ING and have since transferred the funds back to my checking account. MY HSBC account is now up, running, and set to go and I just need to call and have them fax me the beneficiary form so I can fill it out and fax it back. Then I will transfer the $4K back and out of “harms way.”

Investments: I invested another $100 with Sharebuilder and that account is building nicely. We have to start somewhere right? In October, I deposited another $100 and should get the $50 and $25 bonuses in the coming weeks to add to my accounts as well.

Retirement: My 401k performed much better and almost doubled my contributions for the month. Oh yeah! My friend is a financial advisor so he did a new asset allocation for me and it is working out well.

Debt: Student loan interest continues to stack up and capitalize. I am grateful that this is my last year of law school so I can start paying some of this debt off soon.

General comments: Overall, a slight dip in net worth but nothing like last month. It will suffer another dip in January with my last tuition bill but from there on, it should be smooth sailing to financial freedom. I am still interviewing and have another interview this week. I am waiting to hear back from 2 firms that I interviewed with in September. Both are long shots but I am just as deserving as the next, hungry for the opportunity, and know that I can do a great job for whoever hires me. What is meant to be will be, I just have to continue to put my best foot forward.

{kind=link}